Fraud Detection Explained: Definition, Process, and Why It Matters for Businesses

In today’s digital-first world, financial transactions happen in seconds — but so do fraudulent activities. From online banking scams to identity theft and payment fraud, businesses face growing risks every day. That’s where fraud detection plays a crucial role.

Let’s explore what fraud detection is, how it works, and why it has become essential for modern organizations.

What Is Fraud Detection?

Fraud detection is the process of identifying suspicious or illegal activities within transactions, accounts, or systems. It uses technology, data analysis, and behavioral monitoring to detect unusual patterns that may indicate fraud.

Fraud detection systems are commonly used in:

- Banking and financial services

- E-commerce platforms

- Insurance companies

- Telecom services

- Healthcare systems

The goal is simple: prevent financial loss and protect both businesses and customers.

Why Fraud Detection Is Important

Fraud can cause serious consequences, including:

- Financial losses

- Legal penalties

- Damaged brand reputation

- Loss of customer trust

With increasing digital payments and online transactions, fraud attempts have become more sophisticated. Companies can no longer rely on manual monitoring — automated fraud detection systems are now essential.

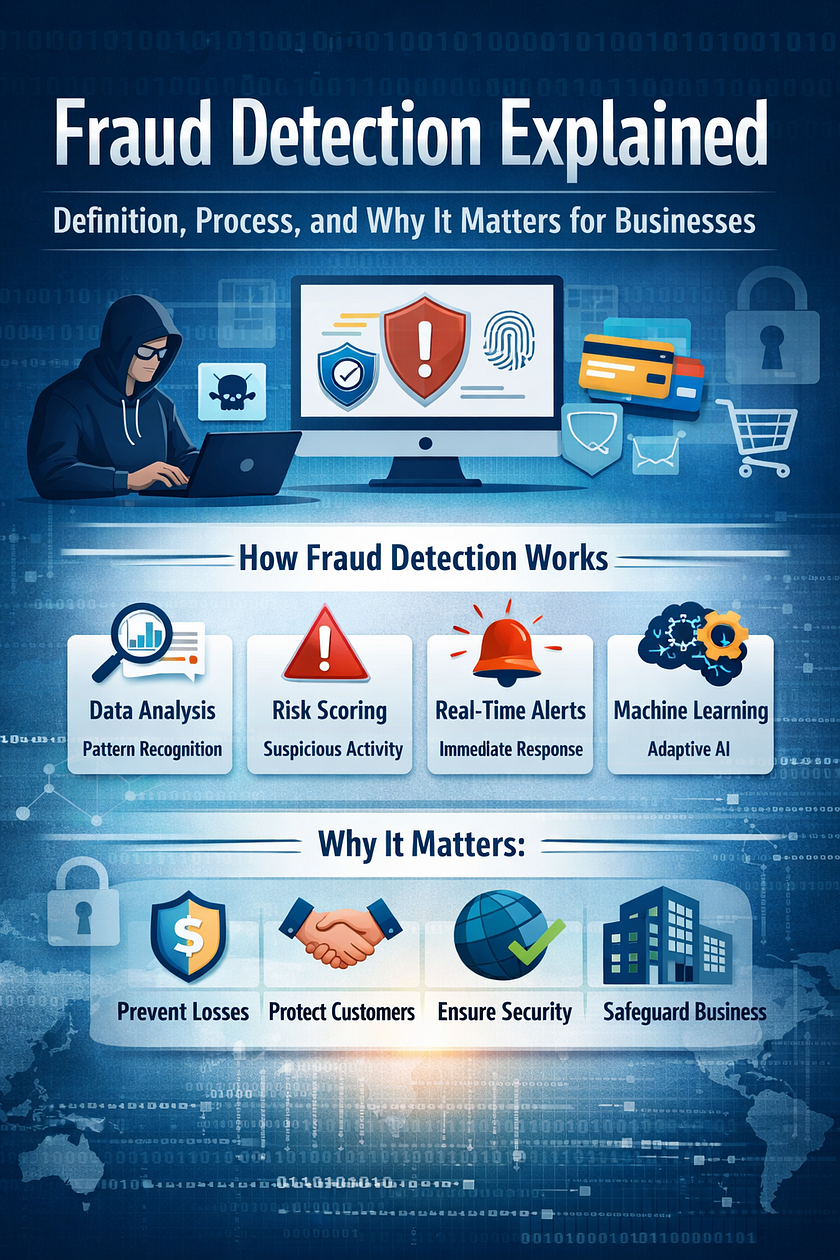

How Fraud Detection Works

Fraud detection systems operate through a combination of data collection, pattern recognition, and real-time monitoring. Here’s a step-by-step breakdown:

1. Data Collection

The system gathers data from multiple sources such as transaction records, login attempts, device information, IP addresses, and customer behavior history.

2. Pattern Analysis

The system analyzes this data to identify patterns. For example:

- Sudden large transactions

- Multiple failed login attempts

- Transactions from unusual locations

- Irregular purchasing behavior

If a transaction deviates from a customer’s typical pattern, it may be flagged as suspicious.

3. Risk Scoring

Each transaction is assigned a risk score based on predefined rules or AI-driven models. A higher risk score indicates a greater likelihood of fraud.

4. Real-Time Alerts

If a transaction crosses a risk threshold, the system can:

- Block the transaction

- Send alerts to security teams

- Request additional customer verification (OTP, 2FA)

- Temporarily freeze the account

This ensures immediate action before financial damage occurs.

5. Continuous Learning

Modern fraud detection systems use machine learning algorithms. These systems improve over time by learning from past fraud cases and adapting to new fraud techniques.

Types of Fraud Detection Methods

Rule-Based Systems

These systems rely on predefined rules, such as blocking transactions above a certain amount or from high-risk countries.

Advantage: Simple and fast

Limitation: Cannot detect new or complex fraud patterns

Machine Learning Models

AI-powered systems analyze vast amounts of historical data to identify unusual patterns and predict fraud risk.

Advantage: Adaptive and accurate

Limitation: Requires high-quality data

Behavioral Analytics

This method monitors user behavior, such as typing speed, device usage, or transaction habits, to detect anomalies.

Biometric Authentication

Some advanced systems use fingerprint scans, facial recognition, or voice authentication to verify identity and prevent fraud.

Key Industries Using Fraud Detection

Banking & Financial Services

Prevents credit card fraud, money laundering, and unauthorized transactions.

E-Commerce

Detects fake orders, payment fraud, and account takeovers.

Insurance

Identifies fraudulent claims and document manipulation.

Telecom

Prevents SIM swap fraud and subscription scams.

Benefits of Effective Fraud Detection

✔ Reduces financial losses

✔ Improves customer trust

✔ Enhances regulatory compliance

✔ Protects brand reputation

✔ Enables secure digital growth

Businesses that invest in strong fraud detection systems create safer customer experiences and long-term sustainability.

Challenges in Fraud Detection

Despite technological advancements, fraud detection still faces challenges:

- False positives (legitimate transactions flagged as fraud)

- Evolving fraud tactics

- High implementation costs

- Data privacy concerns

To overcome these challenges, companies combine AI, analytics, and human oversight.

The Future of Fraud Detection

The future of fraud detection lies in:

- Advanced AI and predictive analytics

- Real-time transaction monitoring

- Multi-layered security frameworks

- Integration with customer experience platforms

As cybercrime continues to evolve, fraud detection systems must stay ahead with smarter, faster, and more adaptive technology.

Final Thoughts

Fraud detection is no longer optional — it is a critical business necessity. In an era of digital transactions and online services, companies must proactively identify threats before they cause damage.

By combining data analytics, machine learning, and intelligent monitoring systems, businesses can safeguard their operations, protect customers, and build long-term trust.

Comments

Post a Comment